Predicting Credit Card Default - Classification

Context

The dataset used for this notebook is from https://archive.ics.uci.edu/ml/datasets/default+of+credit+card+clients or you can check it in https://www.kaggle.com/uciml/default-of-credit-card-clients-dataset/discussion/34608.

Attribute Information:

This research employed a binary variable, default payment (Yes = 1, No = 0), as the response variable. This study reviewed the literature and used the following 23 variables as explanatory variables:

- X1: Amount of the given credit (NT dollar): it includes both the individual consumer credit and his/her family (supplementary) credit.

- X2: Gender (1 = male; 2 = female).

- X3: Education (1 = graduate school; 2 = university; 3 = high school; 4 = others).

- X4: Marital status (1 = married; 2 = single; 3 = others).

- X5: Age (year).

- X6 - X11: History of past payment. We tracked the past monthly payment records (from April to September, 2005) as follows: X6 = the repayment status in September, 2005; X7 = the repayment status in August, 2005; . . .;X11 = the repayment status in April, 2005. The measurement scale for the repayment status is: -1 = pay duly; 1 = payment delay for one month; 2 = payment delay for two months; . . .; 8 = payment delay for eight months; 9 = payment delay for nine months and above.

- X12-X17: Amount of bill statement (NT dollar). X12 = amount of bill statement in September, 2005; X13 = amount of bill statement in August, 2005; . . .; X17 = amount of bill statement in April, 2005.

- X18-X23: Amount of previous payment (NT dollar). X18 = amount paid in September, 2005; X19 = amount paid in August, 2005; . . .;X23 = amount paid in April, 2005.

Importing all packages

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import numpy as np

import seaborn as sns

from scipy.stats import shapiro, mannwhitneyu, chi2_contingency

import ppscore as pps

from sklearn.model_selection import train_test_split, RandomizedSearchCV

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import OneHotEncoder

from sklearn.compose import ColumnTransformer

from sklearn.ensemble import AdaBoostClassifier

from sklearn.neighbors import KNeighborsClassifier

from xgboost import XGBClassifier

from sklearn.svm import SVC

from sklearn.metrics import confusion_matrix, f1_score, roc_auc_score, matthews_corrcoef, precision_score, recall_score, accuracy_score

from jcopml.tuning import random_search_params as rsp

from jcopml.tuning.space import Real, Integer

from yellowbrick.model_selection import LearningCurve

import warnings

warnings.filterwarnings("ignore")

sns.set_style('whitegrid')

cc = pd.read_csv('UCI_Credit_Card.csv')

cc.shape

(30000, 25)

This dataset contains 30.000 observations with 25 features.

cc.head()

| ID | LIMIT_BAL | SEX | EDUCATION | MARRIAGE | AGE | PAY_0 | PAY_2 | PAY_3 | PAY_4 | ... | BILL_AMT4 | BILL_AMT5 | BILL_AMT6 | PAY_AMT1 | PAY_AMT2 | PAY_AMT3 | PAY_AMT4 | PAY_AMT5 | PAY_AMT6 | default.payment.next.month | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 20000.0 | 2 | 2 | 1 | 24 | 2 | 2 | -1 | -1 | ... | 0.0 | 0.0 | 0.0 | 0.0 | 689.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1 |

| 1 | 2 | 120000.0 | 2 | 2 | 2 | 26 | -1 | 2 | 0 | 0 | ... | 3272.0 | 3455.0 | 3261.0 | 0.0 | 1000.0 | 1000.0 | 1000.0 | 0.0 | 2000.0 | 1 |

| 2 | 3 | 90000.0 | 2 | 2 | 2 | 34 | 0 | 0 | 0 | 0 | ... | 14331.0 | 14948.0 | 15549.0 | 1518.0 | 1500.0 | 1000.0 | 1000.0 | 1000.0 | 5000.0 | 0 |

| 3 | 4 | 50000.0 | 2 | 2 | 1 | 37 | 0 | 0 | 0 | 0 | ... | 28314.0 | 28959.0 | 29547.0 | 2000.0 | 2019.0 | 1200.0 | 1100.0 | 1069.0 | 1000.0 | 0 |

| 4 | 5 | 50000.0 | 1 | 2 | 1 | 57 | -1 | 0 | -1 | 0 | ... | 20940.0 | 19146.0 | 19131.0 | 2000.0 | 36681.0 | 10000.0 | 9000.0 | 689.0 | 679.0 | 0 |

5 rows × 25 columns

pd.DataFrame({'dataFeatures' : cc.columns, 'dataType' : cc.dtypes.values,

'null' : [cc[i].isna().sum() for i in cc.columns],

'nullPct' : [((cc[i].isna().sum()/len(cc[i]))*100).round(2) for i in cc.columns],

'Nunique' : [cc[i].nunique() for i in cc.columns],

'uniqueSample' : [list(pd.Series(cc[i].unique()).sample(2)) for i in cc.columns]}).reset_index(drop = True)

| dataFeatures | dataType | null | nullPct | Nunique | uniqueSample | |

|---|---|---|---|---|---|---|

| 0 | ID | int64 | 0 | 0.0 | 30000 | [24194, 23057] |

| 1 | LIMIT_BAL | float64 | 0 | 0.0 | 81 | [40000.0, 110000.0] |

| 2 | SEX | int64 | 0 | 0.0 | 2 | [2, 1] |

| 3 | EDUCATION | int64 | 0 | 0.0 | 7 | [5, 4] |

| 4 | MARRIAGE | int64 | 0 | 0.0 | 4 | [3, 2] |

| 5 | AGE | int64 | 0 | 0.0 | 56 | [61, 30] |

| 6 | PAY_0 | int64 | 0 | 0.0 | 11 | [7, 1] |

| 7 | PAY_2 | int64 | 0 | 0.0 | 11 | [-1, 5] |

| 8 | PAY_3 | int64 | 0 | 0.0 | 11 | [8, 2] |

| 9 | PAY_4 | int64 | 0 | 0.0 | 11 | [6, 0] |

| 10 | PAY_5 | int64 | 0 | 0.0 | 10 | [-2, 0] |

| 11 | PAY_6 | int64 | 0 | 0.0 | 10 | [4, 6] |

| 12 | BILL_AMT1 | float64 | 0 | 0.0 | 22723 | [105105.0, 7065.0] |

| 13 | BILL_AMT2 | float64 | 0 | 0.0 | 22346 | [7277.0, 94153.0] |

| 14 | BILL_AMT3 | float64 | 0 | 0.0 | 22026 | [7251.0, 76767.0] |

| 15 | BILL_AMT4 | float64 | 0 | 0.0 | 21548 | [5733.0, 11950.0] |

| 16 | BILL_AMT5 | float64 | 0 | 0.0 | 21010 | [45617.0, 41630.0] |

| 17 | BILL_AMT6 | float64 | 0 | 0.0 | 20604 | [84237.0, 67700.0] |

| 18 | PAY_AMT1 | float64 | 0 | 0.0 | 7943 | [14180.0, 66.0] |

| 19 | PAY_AMT2 | float64 | 0 | 0.0 | 7899 | [4070.0, 1450.0] |

| 20 | PAY_AMT3 | float64 | 0 | 0.0 | 7518 | [15413.0, 179.0] |

| 21 | PAY_AMT4 | float64 | 0 | 0.0 | 6937 | [6666.0, 8337.0] |

| 22 | PAY_AMT5 | float64 | 0 | 0.0 | 6897 | [6017.0, 15362.0] |

| 23 | PAY_AMT6 | float64 | 0 | 0.0 | 6939 | [1691.0, 2056.0] |

| 24 | default.payment.next.month | int64 | 0 | 0.0 | 2 | [1, 0] |

No missing values! Before I explore the dataset, I’ll rename the target column first.

cc.rename(columns = {'default.payment.next.month' : 'target'}, inplace = True)

cc.dtypes

ID int64

LIMIT_BAL float64

SEX int64

EDUCATION int64

MARRIAGE int64

AGE int64

PAY_0 int64

PAY_2 int64

PAY_3 int64

PAY_4 int64

PAY_5 int64

PAY_6 int64

BILL_AMT1 float64

BILL_AMT2 float64

BILL_AMT3 float64

BILL_AMT4 float64

BILL_AMT5 float64

BILL_AMT6 float64

PAY_AMT1 float64

PAY_AMT2 float64

PAY_AMT3 float64

PAY_AMT4 float64

PAY_AMT5 float64

PAY_AMT6 float64

target int64

dtype: object

Much better…

Exploration Data Analysis

cc['target'].value_counts(normalize = True)

0 0.7788

1 0.2212

Name: target, dtype: float64

Percentage of default is: 22.12%

Hypothesis Testing

Before we go further, i’ll do significance test first. But significance test required normality test, to know the data whether normally distribute or not. I’ll use shapiro-wilk test to do normality test.

Normality Test

It’s a little bit tricky, we need to know, what features is numerical or categorical.

cc.head()

| ID | LIMIT_BAL | SEX | EDUCATION | MARRIAGE | AGE | PAY_0 | PAY_2 | PAY_3 | PAY_4 | ... | BILL_AMT4 | BILL_AMT5 | BILL_AMT6 | PAY_AMT1 | PAY_AMT2 | PAY_AMT3 | PAY_AMT4 | PAY_AMT5 | PAY_AMT6 | target | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 20000.0 | 2 | 2 | 1 | 24 | 2 | 2 | -1 | -1 | ... | 0.0 | 0.0 | 0.0 | 0.0 | 689.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1 |

| 1 | 2 | 120000.0 | 2 | 2 | 2 | 26 | -1 | 2 | 0 | 0 | ... | 3272.0 | 3455.0 | 3261.0 | 0.0 | 1000.0 | 1000.0 | 1000.0 | 0.0 | 2000.0 | 1 |

| 2 | 3 | 90000.0 | 2 | 2 | 2 | 34 | 0 | 0 | 0 | 0 | ... | 14331.0 | 14948.0 | 15549.0 | 1518.0 | 1500.0 | 1000.0 | 1000.0 | 1000.0 | 5000.0 | 0 |

| 3 | 4 | 50000.0 | 2 | 2 | 1 | 37 | 0 | 0 | 0 | 0 | ... | 28314.0 | 28959.0 | 29547.0 | 2000.0 | 2019.0 | 1200.0 | 1100.0 | 1069.0 | 1000.0 | 0 |

| 4 | 5 | 50000.0 | 1 | 2 | 1 | 57 | -1 | 0 | -1 | 0 | ... | 20940.0 | 19146.0 | 19131.0 | 2000.0 | 36681.0 | 10000.0 | 9000.0 | 689.0 | 679.0 | 0 |

5 rows × 25 columns

numerical = ['LIMIT_BAL', 'AGE', 'BILL_AMT1', 'BILL_AMT2', 'BILL_AMT3',

'BILL_AMT4', 'BILL_AMT5', 'BILL_AMT6', 'PAY_AMT1', 'PAY_AMT2',

'PAY_AMT3', 'PAY_AMT4', 'PAY_AMT5', 'PAY_AMT6']

shap = []

for i in numerical:

if shapiro(cc[i])[1] < 0.05:

shap.append('Reject Null Hypothesis')

else:

shap.append('Fail To reject Null Hypothesis')

pd.DataFrame({'Hypothesis' : shap}, index = numerical)

/home/user/anaconda3/lib/python3.7/site-packages/scipy/stats/morestats.py:1681: UserWarning: p-value may not be accurate for N > 5000.

warnings.warn("p-value may not be accurate for N > 5000.")

| Hypothesis | |

|---|---|

| LIMIT_BAL | Reject Null Hypothesis |

| AGE | Reject Null Hypothesis |

| BILL_AMT1 | Reject Null Hypothesis |

| BILL_AMT2 | Reject Null Hypothesis |

| BILL_AMT3 | Reject Null Hypothesis |

| BILL_AMT4 | Reject Null Hypothesis |

| BILL_AMT5 | Reject Null Hypothesis |

| BILL_AMT6 | Reject Null Hypothesis |

| PAY_AMT1 | Reject Null Hypothesis |

| PAY_AMT2 | Reject Null Hypothesis |

| PAY_AMT3 | Reject Null Hypothesis |

| PAY_AMT4 | Reject Null Hypothesis |

| PAY_AMT5 | Reject Null Hypothesis |

| PAY_AMT6 | Reject Null Hypothesis |

Significance Test

Let’s do mannwhitneyu Test then…

mann = []

for i in numerical:

if mannwhitneyu(cc[cc['target'] == 0][i],cc[cc['target'] == 1][i])[1] < 0.05:

mann.append('Reject Null Hypothesis')

else:

mann.append('Fail To Reject Null Hypothesis')

pd.DataFrame(mann, columns = ['Hypothesis'], index = numerical)

| Hypothesis | |

|---|---|

| LIMIT_BAL | Reject Null Hypothesis |

| AGE | Fail To Reject Null Hypothesis |

| BILL_AMT1 | Reject Null Hypothesis |

| BILL_AMT2 | Reject Null Hypothesis |

| BILL_AMT3 | Reject Null Hypothesis |

| BILL_AMT4 | Fail To Reject Null Hypothesis |

| BILL_AMT5 | Fail To Reject Null Hypothesis |

| BILL_AMT6 | Fail To Reject Null Hypothesis |

| PAY_AMT1 | Reject Null Hypothesis |

| PAY_AMT2 | Reject Null Hypothesis |

| PAY_AMT3 | Reject Null Hypothesis |

| PAY_AMT4 | Reject Null Hypothesis |

| PAY_AMT5 | Reject Null Hypothesis |

| PAY_AMT6 | Reject Null Hypothesis |

Chi2 Test

for i in ['ID', 'target']:

numerical.append(i)

categorical = cc.drop(numerical, axis = 1).columns

chi2 = []

for i in categorical:

if chi2_contingency(pd.crosstab(cc['target'], cc[i]))[1] < 0.05:

chi2.append('Reject Null Hypothesis')

else:

chi2.append('Fail To Reject Null Hypothesis')

pd.DataFrame({'Hypothesis' : chi2}, index = categorical)

| Hypothesis | |

|---|---|

| SEX | Reject Null Hypothesis |

| EDUCATION | Reject Null Hypothesis |

| MARRIAGE | Reject Null Hypothesis |

| PAY_0 | Reject Null Hypothesis |

| PAY_2 | Reject Null Hypothesis |

| PAY_3 | Reject Null Hypothesis |

| PAY_4 | Reject Null Hypothesis |

| PAY_5 | Reject Null Hypothesis |

| PAY_6 | Reject Null Hypothesis |

From the significance test, we know AGE and amount of bill statement in June, May, and April are not significance (difference). My recommendation, focus on amount of bill statement in September, August, and July.

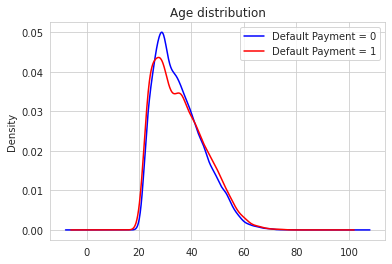

Wait, AGE is not significance? That’s interesting. But why? I thought, younger people will defaulting more. Let’s visualize it.

cc[cc['target'] == 0]['AGE'].plot(kind = 'kde', color = 'blue', label = 'Default Payment = 0')

cc[cc['target'] == 1]['AGE'].plot(kind = 'kde', color = 'red', label = 'Default Payment = 1')

plt.legend()

plt.title('Age distribution')

Text(0.5, 1.0, 'Age distribution')

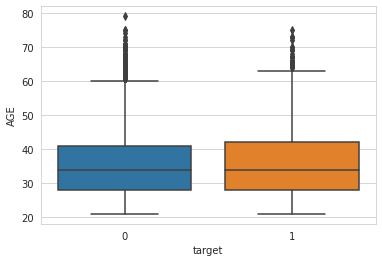

sns.boxplot(y = cc['AGE'], x = cc['target'])

<matplotlib.axes._subplots.AxesSubplot at 0x7f0d46488fd0>

Oh! I see! Almost no difference at all in age distributions between defaulters and not. That’s so suprising. Thanks to Significance Test.

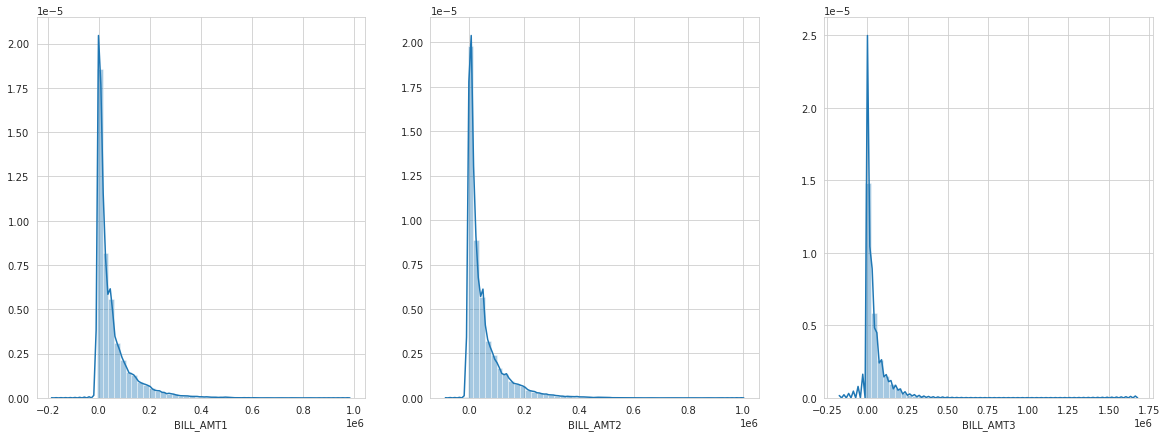

fig, ax = plt.subplots(1, 3, figsize = (20, 7))

for i,j in zip(ax.flatten(), ['BILL_AMT1', 'BILL_AMT2', 'BILL_AMT3']):

sns.distplot(cc[j], ax = i)

The pattern between amount of bill statement in September, August, and July looks same. And that’s make sense, most people don’t want have too much debt and the vast majority of people have debt below about NT$ 50.000. How about the limit balanced? Let me guess, I think, people with lower limit balanced are more likely defaulting. Prove me wrong please…

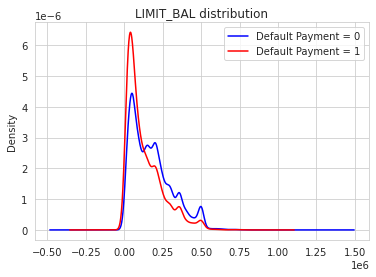

cc[cc['target'] == 0]['LIMIT_BAL'].plot(kind = 'kde', color = 'blue', label = 'Default Payment = 0')

cc[cc['target'] == 1]['LIMIT_BAL'].plot(kind = 'kde', color = 'red', label = 'Default Payment = 1')

plt.legend()

plt.title('LIMIT_BAL distribution')

Text(0.5, 1.0, 'LIMIT_BAL distribution')

:( it’s not suprising at all. The lower limit balanced are more likely defaulting then people with higher limit balanced. Why this make sense? Cause If bank seems ‘don’t trust’ you or they see you’re a ‘high risk’ applicant, bank usually will only give you a smaller line of credit. Does education significance (quantitively)?

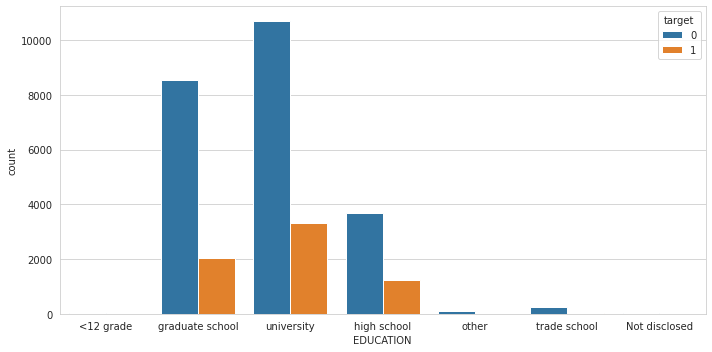

plt.figure(figsize = (10, 5))

sns.countplot(cc['EDUCATION'], hue = cc['target'])

plt.xticks((0,1,2,3,4,5,6),('<12 grade','graduate school','university',

'high school','other','trade school','Not disclosed'))

plt.tight_layout()

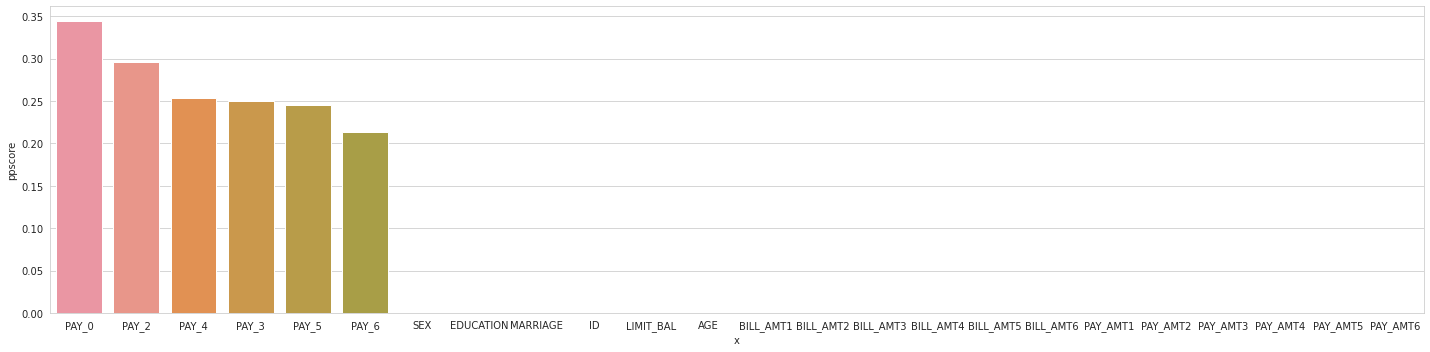

In this observations, our debtors are mostly educated people. Let’s do feature selection using Predictive Power Scoring…

plt.figure(figsize = (20, 5))

df_predictors = pps.predictors(cc, y="target")

sns.barplot(data=df_predictors, x="x", y="ppscore")

plt.tight_layout()

That’s interesting, history of payment features will help model to predictive whether the debtors will defaulting or not.

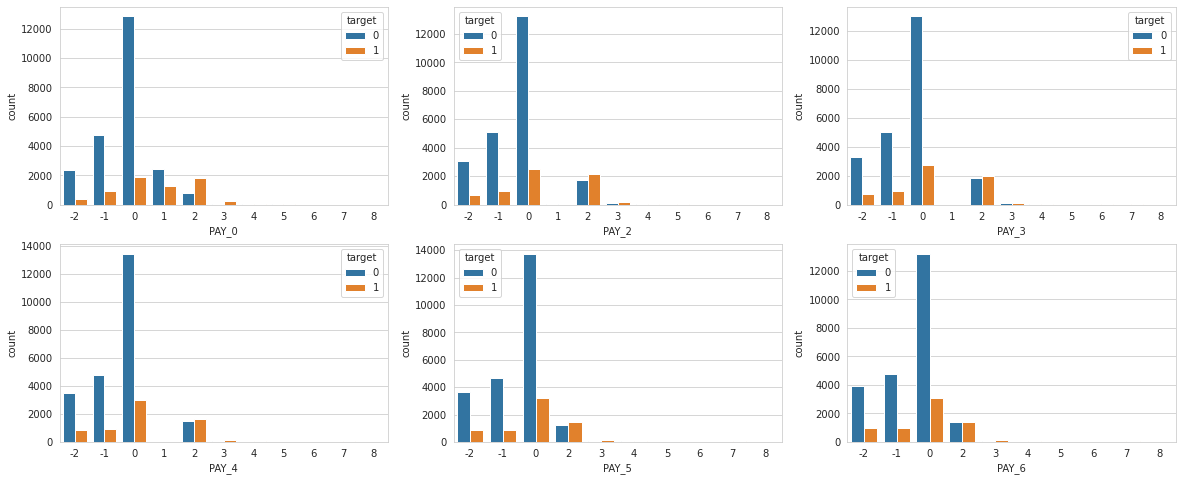

fig, ax = plt.subplots(2,3, figsize = (20, 8))

for i,j in zip([0,2,3,4,5,6],ax.flatten()):

sns.countplot(cc['PAY_{}'.format(i)], hue = cc['target'], ax = j)

Seems they all look same. This plot tell us, that not everyone pays their debt on time. But for the debtors that are already late in a few monts, it looks like they’re more likely to end up in default than debtors who end up paying off their debt.

Splitting Dataset

X = cc.drop(columns = 'target')

y = cc['target']

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size = 0.2, random_state = 101, stratify = y)

X_train.shape, X_test.shape, y_train.shape, y_test.shape

((24000, 24), (6000, 24), (24000,), (6000,))

Preprocessing

categorical = Pipeline([

('onehot', OneHotEncoder(handle_unknown = 'ignore'))

])

preprocessor = ColumnTransformer([

('cat', categorical, ['PAY_{}'.format(i) for i in [0,2,3,4,5,6]])

])

Modeling

def evaluationMetrics(y_test, y_pred):

f1.append(f1_score(y_test,y_pred))

prec.append(precision_score(y_test, y_pred))

recall.append(recall_score(y_test, y_pred))

auc.append(roc_auc_score(y_test, y_pred))

acc.append(accuracy_score(y_test, y_pred))

matthews.append(matthews_corrcoef(y_test, y_pred))

metric = pd.DataFrame(index = ['AdaBoost Classifier', 'KNN Classifier', 'XGBoost Classifier'])

f1 = []

prec = []

recall = []

matthews = []

auc = []

acc = []

Adaboost

ada_params = {

'algo__learning_rate': Real(low=-2, high=0, prior='log-uniform'),

'algo__n_estimators': Integer(low=100, high=200)

}

pipeline = Pipeline([

('prep', preprocessor),

('algo', AdaBoostClassifier())

])

ada = RandomizedSearchCV(pipeline, ada_params, cv = 3, n_jobs = -1, random_state = 101)

ada.fit(X_train, y_train)

print(ada.best_params_)

print(ada.score(X_train, y_train), ada.best_score_, ada.score(X_test, y_test))

{'algo__learning_rate': 0.36122336008063605, 'algo__n_estimators': 105}

0.8197083333333334 0.8192083333333334 0.8256666666666667

y_pred_ada = ada.best_estimator_.predict(X_test)

evaluationMetrics(y_test, y_pred_ada)

KNN

knn_params = {

'algo__n_neighbors': Integer(low=1, high=20),

}

pipeline = Pipeline([

('prep', preprocessor),

('algo', KNeighborsClassifier())

])

knn = RandomizedSearchCV(pipeline, knn_params, cv = 3, n_jobs = -1, random_state = 101)

knn.fit(X_train, y_train)

print(knn.best_params_)

print(knn.score(X_train, y_train), knn.best_score_, knn.score(X_test, y_test))

{'algo__n_neighbors': 16}

0.8184166666666667 0.8162916666666667 0.8191666666666667

y_pred_knn = knn.best_estimator_.predict(X_test)

evaluationMetrics(y_test, y_pred_knn)

XGBoost Classifier

pipeline = Pipeline([

('prep', preprocessor),

('algo', XGBClassifier())

])

xgb = RandomizedSearchCV(pipeline, rsp.xgb_params, cv = 3, n_jobs = -1, random_state = 101)

xgb.fit(X_train, y_train)

print(xgb.best_params_)

print(xgb.score(X_train, y_train), xgb.best_score_, xgb.score(X_test, y_test))

{'algo__colsample_bytree': 0.14363608368376052, 'algo__gamma': 8, 'algo__learning_rate': 0.4501489968769524, 'algo__max_depth': 9, 'algo__n_estimators': 162, 'algo__reg_alpha': 0.2573510611415207, 'algo__reg_lambda': 0.23179283837105844, 'algo__subsample': 0.5208429341570253}

0.821125 0.8199166666666667 0.8258333333333333

y_pred_xgb = xgb.best_estimator_.predict(X_test)

evaluationMetrics(y_test, y_pred_xgb)

Evaluation

Metrics

metric['F1'] = f1

metric['Precision'] = prec

metric['Recall'] = recall

metric['MCC'] = matthews

metric['AUC'] = auc

metric['accuracy'] = acc

metric

| F1 | Precision | Recall | MCC | AUC | accuracy | |

|---|---|---|---|---|---|---|

| AdaBoost Classifier | 0.485236 | 0.699291 | 0.371515 | 0.420359 | 0.663074 | 0.825667 |

| KNN Classifier | 0.440433 | 0.697712 | 0.321778 | 0.386976 | 0.641095 | 0.819167 |

| XGBoost Classifier | 0.490989 | 0.694215 | 0.379804 | 0.422884 | 0.666149 | 0.825833 |

Confusion Matrix

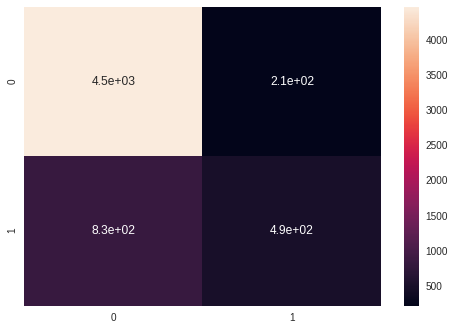

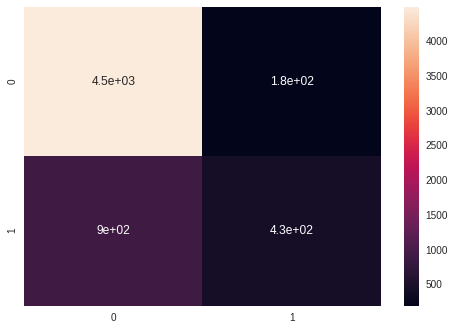

Adaboost

sns.heatmap(confusion_matrix(y_test, y_pred_ada), annot = True)

<matplotlib.axes._subplots.AxesSubplot at 0x7f0d341d8c50>

KNN

sns.heatmap(confusion_matrix(y_test, y_pred_knn), annot = True)

<matplotlib.axes._subplots.AxesSubplot at 0x7f0d34202fd0>

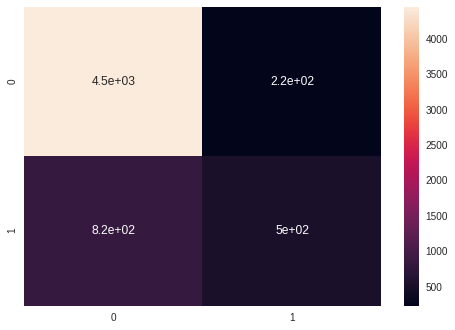

XGBoost

sns.heatmap(confusion_matrix(y_test, y_pred_xgb), annot = True)

<matplotlib.axes._subplots.AxesSubplot at 0x7f0d342ade90>

Learning Curves

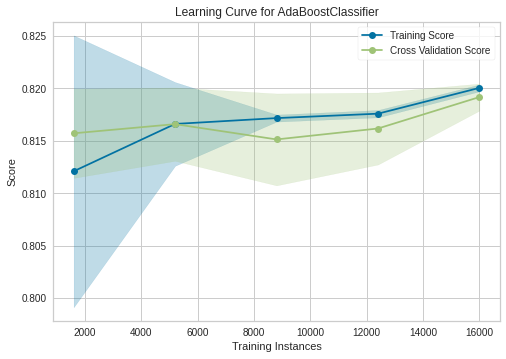

Adaboost

sizes = np.linspace(0.3, 1, 10)

visualizer = LearningCurve(

ada.best_estimator_, scoring = 'accuracy', train_size = sizes, random_state = 101, cv = 3

)

visualizer.fit(X_train, y_train)

visualizer.show()

<matplotlib.axes._subplots.AxesSubplot at 0x7f0d3440df90>

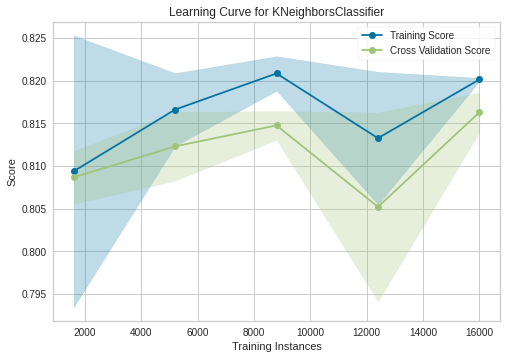

KNN

sizes = np.linspace(0.3, 1, 10)

visualizer = LearningCurve(

knn.best_estimator_, scoring = 'accuracy', train_size = sizes, random_state = 101, cv = 3

)

visualizer.fit(X_train, y_train)

visualizer.show()

<matplotlib.axes._subplots.AxesSubplot at 0x7f0d343f6790>

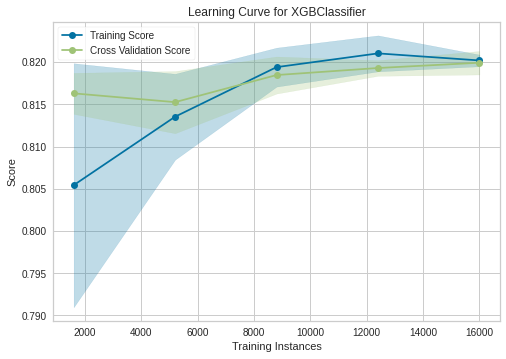

XGBoost

sizes = np.linspace(0.3, 1, 10)

visualizer = LearningCurve(

xgb.best_estimator_, scoring = 'accuracy', train_size = sizes, random_state = 101, cv = 3

)

visualizer.fit(X_train, y_train)

visualizer.show()

<matplotlib.axes._subplots.AxesSubplot at 0x7f0d342f7c50>

Conclusion

Our best model is XGBoost with 82-83% accuracy and if we see to his learning curve, its a good fit.