Fraud Detection on Bank Payments - Classification

Context

This Dataset taken from Kaggle

Original paper

Lopez-Rojas, Edgar Alonso ; Axelsson, Stefan Banksim: A bank payments simulator for fraud detection research Inproceedings 26th European Modeling and Simulation Symposium, EMSS 2014, Bordeaux, France, pp. 144–152, Dime University of Genoa, 2014, ISBN: 9788897999324. https://www.researchgate.net/publication/265736405_BankSim_A_Bank_Payment_Simulation_for_Fraud_Detection_Research

Attributes Information

Step: This feature represents the day from the start of simulation.

It has 180 steps so simulation ran for virtually 6 months.

Customer: This feature represents the customer id

Age: Categorized age

0: <= 18,

1: 19-25,

2: 26-35,

3: 36-45,

4: 46-55,

5: 56-65,

6: > 65

U: Unknown

zipCodeOrigin: The zip code of origin/source.

Merchant: The merchant's id

zipMerchant: The merchant's zip code

Gender: Gender for customer

E : Enterprise,

F: Female,

M: Male,

U: Unknown

Category: Category of the purchase.

Amount: Amount of the purchase

Fraud: Target variable which shows if the transaction fraudulent(1) or benign(0)

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import re

import ppscore as pps

from imblearn.pipeline import Pipeline

from imblearn.over_sampling import SMOTE

from imblearn.under_sampling import NearMiss

from sklearn.preprocessing import StandardScaler, OneHotEncoder

from sklearn.compose import ColumnTransformer

from sklearn.metrics import classification_report, average_precision_score

import warnings

warnings.filterwarnings('ignore')

from sklearn.linear_model import LogisticRegression

from sklearn.ensemble import RandomForestClassifier

from sklearn.model_selection import RandomizedSearchCV, train_test_split, GridSearchCV

from jcopml.tuning import random_search_params as rsp

from jcopml.tuning.space import Real, Integer

from jcopml.plot import plot_pr_curve

from xgboost import XGBClassifier

sns.set_style('whitegrid')

df = pd.read_csv('bs140513_032310.csv')

df.shape

(594643, 10)

It’s a huge dataset.

df.head()

| step | customer | age | gender | zipcodeOri | merchant | zipMerchant | category | amount | fraud | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 'C1093826151' | '4' | 'M' | '28007' | 'M348934600' | '28007' | 'es_transportation' | 4.55 | 0 |

| 1 | 0 | 'C352968107' | '2' | 'M' | '28007' | 'M348934600' | '28007' | 'es_transportation' | 39.68 | 0 |

| 2 | 0 | 'C2054744914' | '4' | 'F' | '28007' | 'M1823072687' | '28007' | 'es_transportation' | 26.89 | 0 |

| 3 | 0 | 'C1760612790' | '3' | 'M' | '28007' | 'M348934600' | '28007' | 'es_transportation' | 17.25 | 0 |

| 4 | 0 | 'C757503768' | '5' | 'M' | '28007' | 'M348934600' | '28007' | 'es_transportation' | 35.72 | 0 |

Exploratory Data Analysis

df.describe()

| step | amount | fraud | |

|---|---|---|---|

| count | 594643.000000 | 594643.000000 | 594643.000000 |

| mean | 94.986827 | 37.890135 | 0.012108 |

| std | 51.053632 | 111.402831 | 0.109369 |

| min | 0.000000 | 0.000000 | 0.000000 |

| 25% | 52.000000 | 13.740000 | 0.000000 |

| 50% | 97.000000 | 26.900000 | 0.000000 |

| 75% | 139.000000 | 42.540000 | 0.000000 |

| max | 179.000000 | 8329.960000 | 1.000000 |

pd.DataFrame({'dataFeatures' : df.columns, 'dataType' : df.dtypes.values,

'null' : [df[i].isna().sum() for i in df.columns],

'nullPct' : [((df[i].isna().sum()/len(df[i]))*100).round(2) for i in df.columns],

'Nunique' : [df[i].nunique() for i in df.columns],

'uniqueSample' : [list(pd.Series(df[i].unique()).sample()) for i in df.columns]}).reset_index(drop = True)

| dataFeatures | dataType | null | nullPct | Nunique | uniqueSample | |

|---|---|---|---|---|---|---|

| 0 | step | int64 | 0 | 0.0 | 180 | [56] |

| 1 | customer | object | 0 | 0.0 | 4112 | ['C1340235335'] |

| 2 | age | object | 0 | 0.0 | 8 | ['3'] |

| 3 | gender | object | 0 | 0.0 | 4 | ['M'] |

| 4 | zipcodeOri | object | 0 | 0.0 | 1 | ['28007'] |

| 5 | merchant | object | 0 | 0.0 | 50 | ['M1294758098'] |

| 6 | zipMerchant | object | 0 | 0.0 | 1 | ['28007'] |

| 7 | category | object | 0 | 0.0 | 15 | ['es_home'] |

| 8 | amount | float64 | 0 | 0.0 | 23767 | [253.67] |

| 9 | fraud | int64 | 0 | 0.0 | 2 | [0] |

df['fraud'].value_counts(normalize = True)

0 0.987892

1 0.012108

Name: fraud, dtype: float64

As we can see, just 1% who fraud the bank payments. Its an highly imbalanced, so I’ll perform SMOTE (Synthetic Minority Over-sampling Technique) in the modeling part. And we need to be careful to choose an evaluation metric, where accuracy and ROC-AUC doesnt work anymore.

I’m a little bit curious, what most selected categories for fraudsters?

df.groupby('category').mean()['fraud']*100

category

'es_barsandrestaurants' 1.882944

'es_contents' 0.000000

'es_fashion' 1.797335

'es_food' 0.000000

'es_health' 10.512614

'es_home' 15.206445

'es_hotelservices' 31.422018

'es_hyper' 4.591669

'es_leisure' 94.989980

'es_otherservices' 25.000000

'es_sportsandtoys' 49.525237

'es_tech' 6.666667

'es_transportation' 0.000000

'es_travel' 79.395604

'es_wellnessandbeauty' 4.759380

Name: fraud, dtype: float64

Looks like leisure and travel category are the most selected categories for fraudsters. But why?

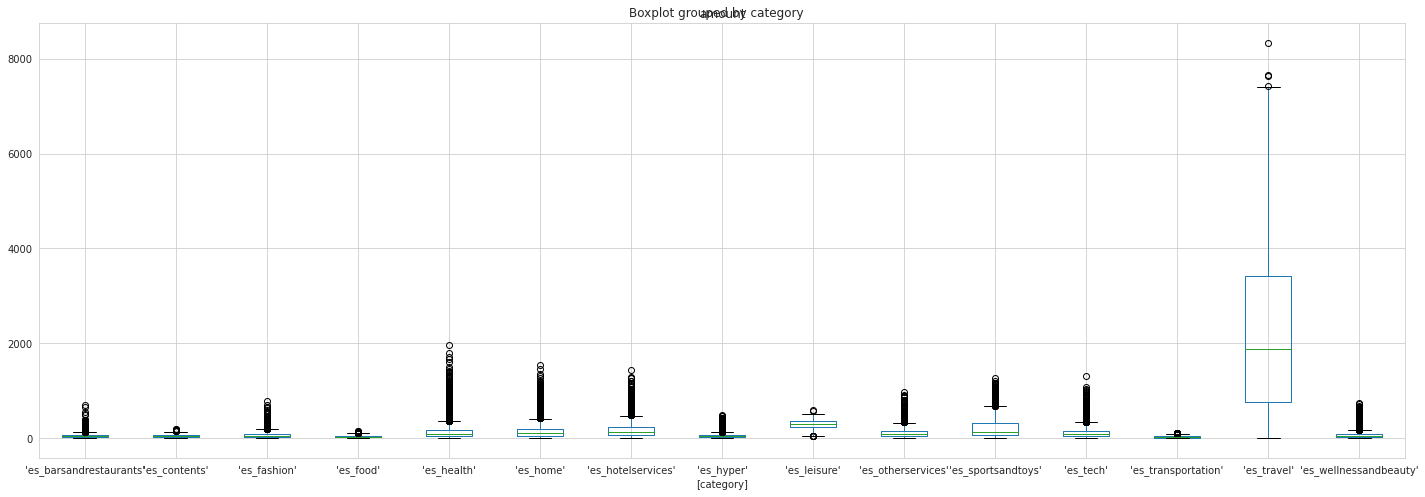

df[['amount', 'category']].boxplot(by = 'category', figsize = (20,7))

plt.tight_layout()

df.groupby('category').mean().sort_values('amount', ascending = False)

| step | amount | fraud | |

|---|---|---|---|

| category | |||

| 'es_travel' | 85.104396 | 2250.409190 | 0.793956 |

| 'es_leisure' | 84.667335 | 288.911303 | 0.949900 |

| 'es_sportsandtoys' | 81.332834 | 215.715280 | 0.495252 |

| 'es_hotelservices' | 92.966170 | 205.614249 | 0.314220 |

| 'es_home' | 89.760322 | 165.670846 | 0.152064 |

| 'es_otherservices' | 70.445175 | 135.881524 | 0.250000 |

| 'es_health' | 100.636211 | 135.621367 | 0.105126 |

| 'es_tech' | 95.034177 | 120.947937 | 0.066667 |

| 'es_fashion' | 95.426092 | 65.666642 | 0.017973 |

| 'es_wellnessandbeauty' | 90.658094 | 65.511221 | 0.047594 |

| 'es_hyper' | 77.837652 | 45.970421 | 0.045917 |

| 'es_contents' | 99.633898 | 44.547571 | 0.000000 |

| 'es_barsandrestaurants' | 75.210576 | 43.461014 | 0.018829 |

| 'es_food' | 107.100861 | 37.070405 | 0.000000 |

| 'es_transportation' | 94.953059 | 26.958187 | 0.000000 |

I see. Leisure and travel are two highest category in amount features. Fraudsters choose the categories which people spend more. And if we see the boxplot, we can see, in the travel category, it can be seen that he has a great variety amount of purchase, it can be one of the reason fraudsters choose this category. He/she will be harder to get caught.

df.groupby('age').mean()['fraud']*100

age

'0' 1.957586

'1' 1.185254

'2' 1.251401

'3' 1.192815

'4' 1.293281

'5' 1.095112

'6' 0.974826

'U' 0.594228

Name: fraud, dtype: float64

That’s smart… Fraudsters using fake identity, with <= 18yo, and as I know, we cannot imprison people under the age of 18. So maybe, Fraudsters think, it would be less consequences if they use fake identity, show how young they are.

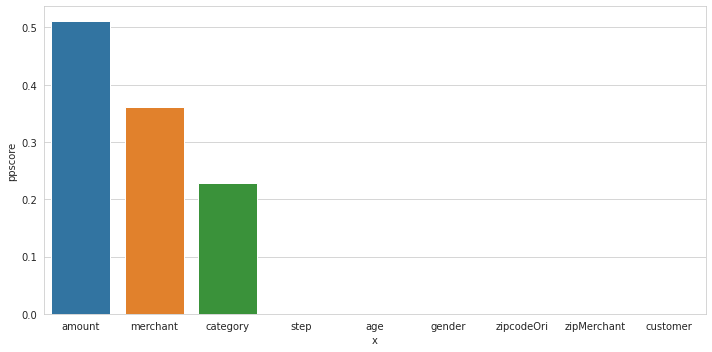

Feature Importances

I’m used Predictive Power Score to do feature selection and to see feature importances.

plt.figure(figsize = (10, 5))

df_predictors = pps.predictors(df, y="fraud")

sns.barplot(data=df_predictors, x="x", y="ppscore")

plt.tight_layout()

Dataset Splitting

X = df.drop(columns= 'fraud')

y = df['fraud']

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, stratify=y, random_state=101)

X_train.shape, X_test.shape, y_train.shape, y_test.shape

((475714, 9), (118929, 9), (475714,), (118929,))

Preprocessing

numerical = Pipeline([

('scaler', StandardScaler())

])

categorical = Pipeline([

('onehot', OneHotEncoder(handle_unknown = 'ignore'))

])

preprocessor = ColumnTransformer([

('numerical', numerical, ['amount']),

('categorical', categorical, ['category', 'merchant', 'age', 'zipMerchant'])

])

Modeling

I’ll perform SMOTE. And my objective is, I want to have a model with high Average Precision Score.

RandomizedSearchCV

Logistic Regresion

logreg_params = {

'algo__fit_intercept': [True, False],

'algo__C': Real(low=-2, high=2, prior='log-uniform')

}

SMOTE

pipeline = Pipeline([

('prep', preprocessor),

('sm', SMOTE(sampling_strategy = 0.8)),

('algo', LogisticRegression(solver='lbfgs', n_jobs=-1, random_state=101))

])

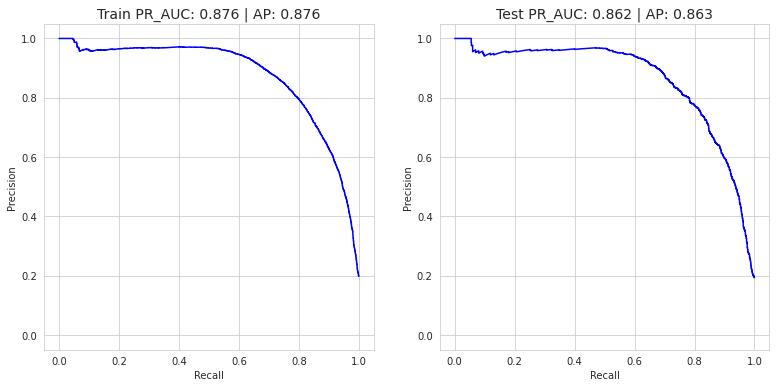

logreg = RandomizedSearchCV(pipeline, logreg_params, cv= 3, scoring= 'average_precision', random_state=101)

logreg.fit(X_train, y_train)

print(logreg.best_params_)

print(logreg.score(X_train, y_train), logreg.best_score_, logreg.score(X_test, y_test))

{'algo__C': 1.3691263238256033, 'algo__fit_intercept': True}

0.8759206521802209 0.8754256285729967 0.862514901182484

y_pred = logreg.best_estimator_.predict(X_test)

print(classification_report(y_test, y_pred))

precision recall f1-score support

0 1.00 0.97 0.99 117489

1 0.30 0.98 0.45 1440

accuracy 0.97 118929

macro avg 0.65 0.97 0.72 118929

weighted avg 0.99 0.97 0.98 118929

plot_pr_curve(X_train, y_train, X_test, y_test, logreg)

Manual Tuning

Unfortunately, I’m not used RandomizedSearchCV for another model except Logistic Regression. The reason is: This is a huge dataset (+ SMOTE) so using RandomizedSearchCV it cost many of time. And I’m not sure my laptop can handle it. So I decided to tuning my model by manually.

Random Forest

rf = Pipeline([

('prep', preprocessor),

('sm', SMOTE(sampling_strategy = 0.8)),

('algo', RandomForestClassifier(n_estimators=150,max_depth=7,random_state=101))

])

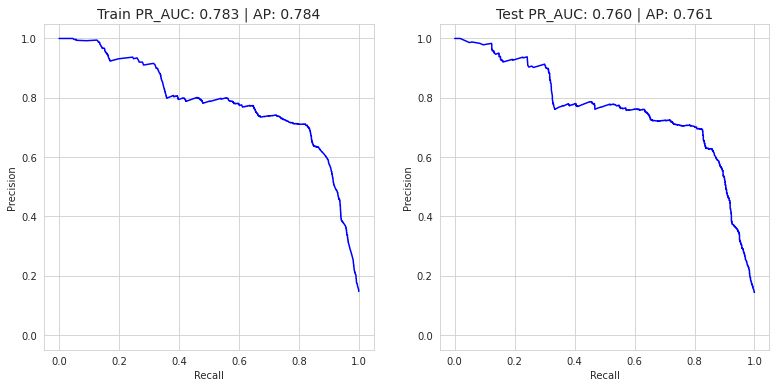

rf.fit(X_train, y_train)

y_pred = rf.predict(X_test)

y_pred_proba = rf.predict_proba(X_test)

print(classification_report(y_test, y_pred))

print('Random Forest Classifier => AP score: {}'.format(average_precision_score(y_test, y_pred_proba[:,1])))

precision recall f1-score support

0 1.00 0.94 0.97 117489

1 0.18 0.99 0.30 1440

accuracy 0.94 118929

macro avg 0.59 0.97 0.63 118929

weighted avg 0.99 0.94 0.96 118929

Random Forest Classifier => AP score: 0.7607888216219187

plot_pr_curve(X_train, y_train, X_test, y_test, rf)

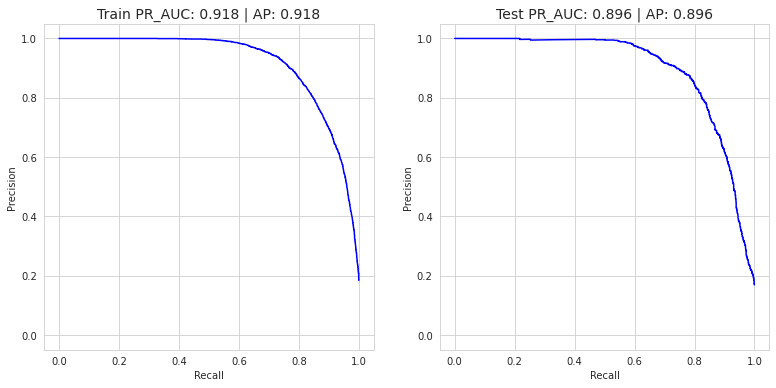

XGBoost

xgb = Pipeline([

('prep', preprocessor),

('sm', SMOTE(sampling_strategy = 0.8)),

('algo', XGBClassifier(max_depth=7, learning_rate=0.08, n_estimators=300,

gamma = 1, subsample= 0.5, colsample_bytree=1, random_state = 101))

])

xgb.fit(X_train, y_train)

y_pred = xgb.predict(X_test)

y_pred_proba = xgb.predict_proba(X_test)

print(classification_report(y_test, y_pred))

print('XGBoost Classifier => AP score: {}'.format(average_precision_score(y_test, y_pred_proba[:,1])))

precision recall f1-score support

0 1.00 0.98 0.99 117489

1 0.35 0.96 0.51 1440

accuracy 0.98 118929

macro avg 0.67 0.97 0.75 118929

weighted avg 0.99 0.98 0.98 118929

XGBoost Classifier => AP score: 0.8957515556626793

plot_pr_curve(X_train, y_train, X_test, y_test, xgb)

Conclusion

Based on AP (Average Precision) Score, we can say, XGBoost Classifier is the best model between Logistic Regression and Random Forest Classifier.